Is It Time to Rotate Out of the Magnificent Seven?

A Systematic Approach

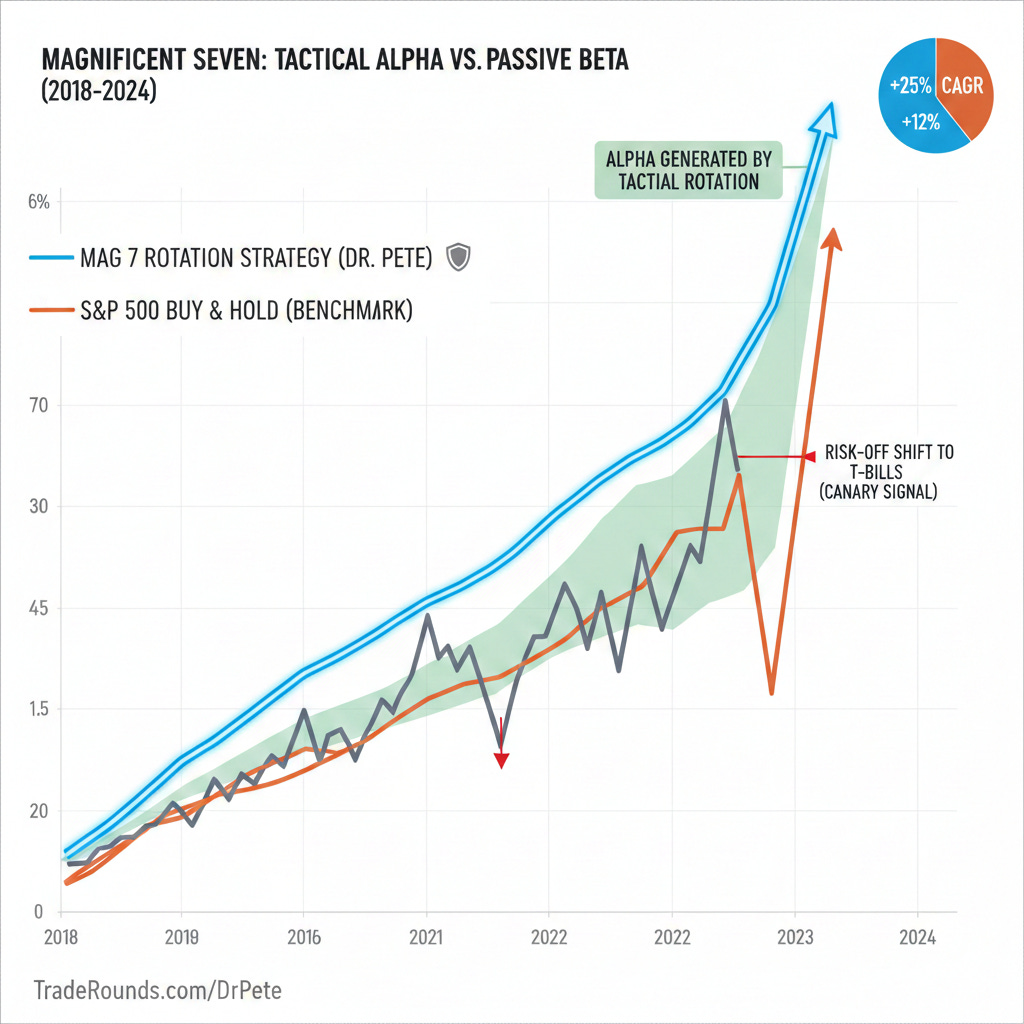

The "Magnificent Seven" (Mag 7) have dominated the market narrative for years, often acting as the sole engine for U.S. equity returns. But for the tactical investor, the biggest risk isn't missing the rally—it’s staying at the party too long after the music stops.

I have just published a new research paper on SSRN titled “A Systematic Momentum-Based Approach to Allocating Between the Magnificent Seven and Broad Equity Indices.” In this study, I apply a quantitative framework to determine exactly when to ride the Mag 7 wave and when to take cover in broad market indices or defensive assets.

The Concentration Risk Dilemma

Most investors are “accidentally” over-concentrated in the Mag 7 through passive index funds. While this was a winning hand in 2023 and parts of 2024, the risk of a “reversion to the mean” is a constant threat.

My research introduces a Dual-Momentum Framework designed to navigate this concentration risk.

The Strategy: Relative Strength meets Regime Awareness

The methodology I developed for this paper focuses on three core pillars:

Relative Momentum: We compare the performance of the Magnificent Seven (via equal-weighted or cap-weighted baskets) against the S&P 500 and Nasdaq-100.

The “Canary” Filter: Using a regime-awareness trigger (similar to the Hybrid Asset Allocation model), the strategy identifies when the broad macro environment is no longer supportive of high-beta growth stocks.

Adaptive Rotation: When momentum is high and the regime is “Risk-On,” the strategy concentrates in the Mag 7. When the trend falters or risk rises, it systematically rotates back to the broader market or defensive T-Bills.

Key Findings from the Study

Enhanced Alpha: By rotating into the Mag 7 only during periods of confirmed relative strength, the strategy significantly outperformed a static “buy and hold” approach to the S&P 500.

Downside Protection: The inclusion of a trend-following filter successfully mitigated the deep drawdowns often associated with concentrated tech positions during market corrections.

Reduced Volatility: The systematic rotation provided a smoother equity curve compared to the “boom or bust” nature of holding concentrated tech leadership indefinitely.

Why This Matters for TradeRounds Followers

Quantitative trading isn’t about guessing which AI stock will double next; it’s about process over prediction. This paper provides a mathematical blueprint for handling the market’s most influential stocks without falling victim to the “concentration trap.”

Read the Full Paper

For the full breakdown of the data, the specific ETFs used in the backtest (including MAGS/METU and SPY/QQQ), and the performance metrics, you can access the complete study here:

Stay disciplined,

Dr. Pete

TradeRounds.com