Beyond the Calendar: Why Your 60/40 Portfolio Needs a "Safety Tripwire"

A Practitioner’s Guide to the Architectural Efficiency of Threshold-Based Rebalancing

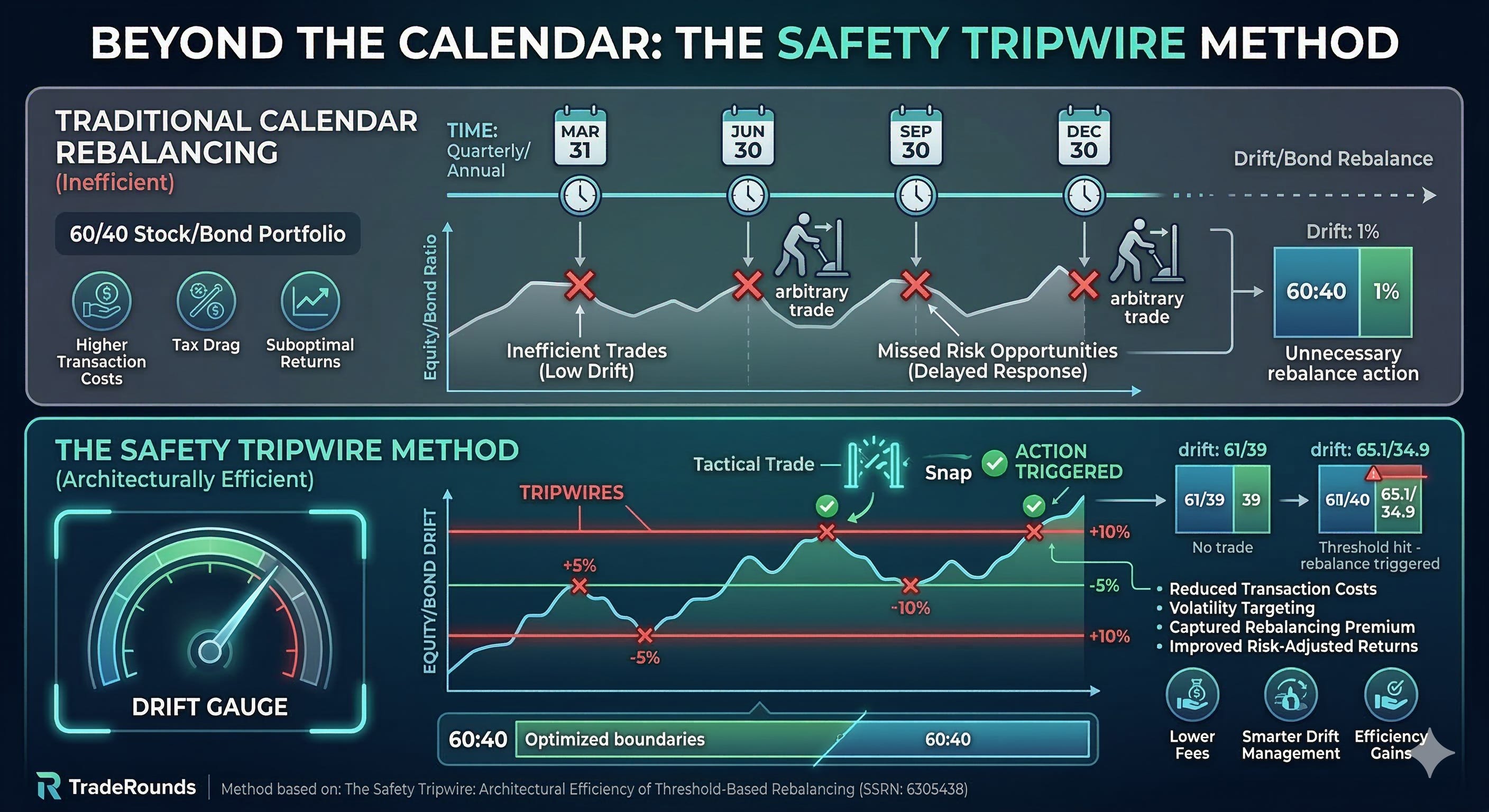

The 60/40 portfolio—60% stocks, 40% bonds—is the bedrock of modern asset allocation. But while the allocation is timeless, the maintenance is often stuck in the past. Most investors rebalance on a rigid schedule: every quarter, or every year, regardless of what the market is actually doing.

In my recent SSRN paper, The Safety Tripwire: Architectural Efficiency of Threshold-Based Rebalancing in a 60/40 Regime, I argue that this “calendar-blind” approach is fundamentally inefficient. To maximize the 60/40’s potential, you need to stop trading the clock and start trading the drift.

The Problem with Calendar Rebalancing

Calendar-based rebalancing (e.g., “I rebalance every December 31st”) assumes the market cares about our Gregorian calendar. It doesn’t. This approach creates two distinct types of architectural waste:

The “Nothing” Trade: You rebalance because the date arrived, even if your portfolio only drifted to 61/39. You pay commissions and spread for a negligible change in risk.

The “Delayed” Trade: A massive market move happens in February, pushing you to 70/30. If you wait until June to rebalance, you’ve spent four months exposed to significantly higher drawdown risk than you intended.

Introducing the “Safety Tripwire”

The “Safety Tripwire” is a threshold-based strategy. Instead of looking at the date, you look at the deviation. You only trigger a trade when the portfolio drifts past a predetermined boundary—for example, a 5% absolute deviation.

In this regime, your 60/40 stays “hands-off” as long as it fluctuates between 55/45 and 65/35. The moment it hits 65.1%, the “tripwire” snaps, and you rebalance back to the 60/40 target.

Why It’s “Architecturally Efficient”

My research highlights that threshold rebalancing isn’t just about “timing”; it’s about architectural efficiency. By moving away from the calendar, you achieve three critical advantages:

Reduced Transaction Costs: By ignoring minor drifts, you execute fewer trades over the long run, saving on slippage and fees.

Capturing the Rebalancing Premium: Thresholds allow the “winners” to run just enough to capture momentum, but force a sell-high/buy-low action precisely when the risk-reward profile has skewed too far.

Volatility Targeting: The Safety Tripwire acts as a mechanical risk-off switch. It forces you to buy bonds during equity crashes and sell stocks during irrational exuberance—not because you “felt” like it, but because the architecture demanded it.

Practical Implementation for Traders

If you’re managing a 60/40 split, you don’t need a complex algorithm to start. You can implement a Safety Tripwire using a simple Python script or even basic platform alerts.

Pro Tip: For most retail portfolios, an absolute threshold of 5% (e.g., rebalancing at 65% stocks) or a relative threshold of 10% of the asset’s weight (e.g., rebalancing when the 60% stock portion hits 66%) provides the best balance between risk control and cost-efficiency.

The 60/40 regime isn’t dead—it just needs a smarter trigger. By replacing your calendar with a Safety Tripwire, you stop being a passenger to time and start being a manager of drift.